Macbooks are the most popular computer right now, but they are well-known for their excessive price. The basic 13-inch MacBook Pro will cost you $1299.00, and you have to spend $2799.00 for a 16-inch high-end.

You may not have that much money in your savings account to purchase your favorite one. In that case, what should you do? You may either prevent yourself from getting a new MacBook Pro, or you have to manage money, right?

Don’t worry! There is still a way to spread out your payment with the passage of time with Macbook financing. In this article, we have demonstrated how you can finance a Macbook Pro following some apple finance options.

Read the entire write-up below, and grab your desired MacBook Pro as early as possible. So, without any further intro, let’s get into the discussion.

How Can I Finance a Macbook Pro?

It is not a good idea to take on debt for purchasing a laptop that you will only use for completing simple tasks, or playing games. If you want to purchase a Macbook Pro for professional purposes that require a high-configuration laptop, then you can go for one.

If you are able to pay in cash for your MacBook Pro, that’s obviously the best option, but if you can’t, then you can go for a number of MacBook pro financing options available.

In this segment, we have demonstrated some of the most common ways to finance your MacBook Pro. Hopefully, you will get some simple solutions regarding it here.

Apple Credit Card

If you own multiple apple products, the apple credit is worth contemplating, because the apple card offers up to 3% cash back on apple products purchase.

The annual fee of Apple credit is 0%, and you will have 2% cash back on other purchases daily if you use your iPhone or Apple watch to pay with an apple card.

Using the Apple Credit Card, you can purchase your new Macbook Pro with interest-free monthly payments. You just need to select the “Apple Card Monthly Installments” and then check out.

Keep in mind that, to use the card, you must own an iPhone or iPad with iOS14.7.1 or later, or iPad.

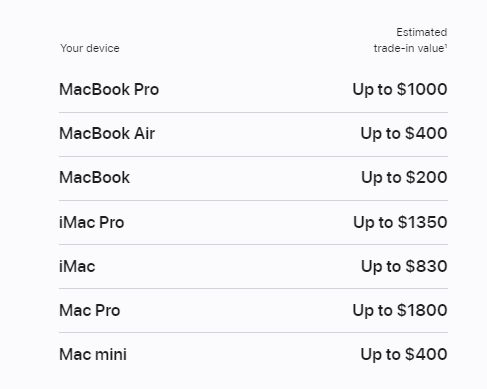

Apple Trade-In

You may be unfamiliar with these three words. Let us explain what Apple Trade-In is. It is a recycling program that makes you able to return your used apple products and get a new one.

In that case, you’ll have a credit towards your next purchase, or a gift card that you will be up to use anytime. By returning your old products, you can shop for a new Mac with your trade-in credit.

One thing you have to remember is that your device must be eligible for the trade-in credit.

Check out the below table to see the estimated trade-in value of your used devices.

Store Credit Cards

The Store Credit Cards are issued by departments or other wholesale stores. They sometimes offer special promotions such as discounts or interest-free periods for shopping in the store.

You can use this credit card in stores or at a branch of that store. Sometimes you’ll be able to use it to buy things anywhere.

The best part is that it is easier to meet the requirements for getting a Store Credit Card Than the traditional one. Besides that, making payments with the card regularly will help you increase your credit score.

But, the Store Cards charge higher interest rates than other options. If no options are left, then you go for this one to make payment for your Macbook Pro.

Traditional Credit Cards

This is one of the easiest ways to finance a MacBook Pro. More than 80% of Americans hold at least a credit card. Using the card means you are borrowing money to pay for your MacBook, and you have to repay the balance over time with a certain interest rate. There is no particular time frame to pay off your card.

Using a Credit Card is the best option for MacBook finance if you can pay off your balance as early as possible. Because the longer you carry the balance, the more interest will go up. So, you have to consider the downward trend of the credit of Traditional credit cards.

But, we still believe that it is easier than other options to finance a Macbook Pro. However, before making the payment, make sure the maximum amount you are allowed to borrow is with your card.

Personal Loan

It is another way to finance your Macbook Pro, but you must have excellent credit to meet the requirement for your best rates. The average interest loan with excellent credit is less than 10 percent depending on the credit score. Check out the below table to know how much interest you have to pay based on your credit score.

| Credit Score | Average Personal Loan Interest Rate |

|---|---|

| 720–850 | 10.3%–12.5% |

| 690–719 | 13.5%–15.5% |

| 630–689 | 17.8%–19.9% |

| 300–629 | 28.5%–32.0% |

The benefit of financing your MacBook Pro with a personal loan is that the monthly payment is fixed; thus, you can simply make your budget on the very first of every month. By making the payment on time, you can enhance your credit score.

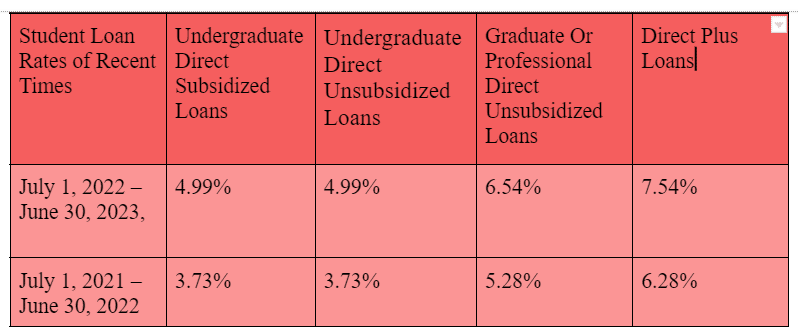

Student Loan

Are you a student who would like to use a MacBook Pro to make your assignments or other academic tasks easier, but can’t afford the cost? There is good news for you. You can take a student loan, and use it to finance your MacBook Pro.

The interest rate is between 3.72% to 6.28% on federal student loans depending on whether you are an undergraduate, graduate, or professional student. You can go for private student loans as well.

Federal student loan rates change every year. We have included the last and the next one-year interest of the student loan here.

Another good news for you if you are a student. If you are a student of a college or post-secondary institution, there is a student discount on your purchase if you directly purchase from Apple. you‘ll have $100 off on any 13-inch MacBook Pro, and $200 on a 16-inch version.

Final Thought

So, this was all about how you can finance a MacBook Pro. We have demonstrated 6 different options that you can follow to make the payment for your desired MacBook.

In short, you can use your Apple Credit Card, Apple Trade-In option, Store Credit Card, Personal Loan, and Traditional Credit Card to finance a MacBook Pro.

If you are still a student, and would like to get a new MacBook, but don’t have sufficient money to pay, you can go for a Student Loan with less interest rate as well.